If you’re launching a startup, you’re likely willing, ready, and hungry for any sort of tips and tricks you can use to save money. Or at least you should be. While it’s a sad statistic, upwards of 9 out of 10 startups end up failing. If you want to be the 1 out of 10 that is successful, you have to keep a sharp focus on finances.

Driving traffic to your YouTube channel, crowdfunding campaigns, and website are important of course, but the financial aspects of the startup are exponentially more critical. If you are considering launching a startup, you’re already in the early stages, or you’re well underway, you owe it to yourself, your employees, and your business as a whole to check out these tips we’ve put together.

1. Cash Flow Management

Running out of money is the number one reason that the majority of those 9 failed startups crash and burn. In order to avoid this pitfall, you need to know where every single dollar is going.

As you get underway, there are going to be both expected and unexpected expenses and you simply have to monitor all spending. Failure to stay on top of this is a recipe for disaster because no matter how awesome your mission statement and company may be, it can all come crashing down if you run out of money.

At a minimum, you should consider hiring a CPA, or better yet, utilizing financial planning software to help ensure success in this area.

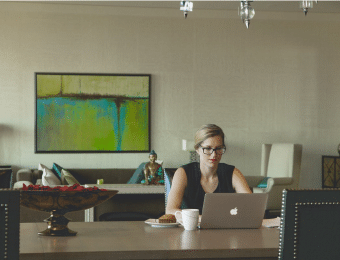

2. Leveraging Work from Home Models

Numerous businesses are utilizing home office options at least in some capacity and for your startup, it could be invaluable. Having non-critical employees/positions slated to work from home can save on office space and actually improve employee morale.

With a VPN and the right equipment, a small investment could net long-term positive results.

While outsourcing received a bad reputation in the past, these days there are a lot of reputable professional organizations in the United States that provide a variety of highly skilled outsourcing services. While recent ransomware attacks may make you leery of outsourcing your IT department, there are non-core duties that are less daunting to outsource.

3. Outsource Where Possible

Outsourcing positions such as HR, payroll, call center services, web development, ordering, inventory, and other functions can save you money while providing you with the quality of work you demand.

You may also consider a pay stub generator to assist with generating paychecks.

4. Prepare for the Worst

This one really goes hand-in-hand with number 1 above because it includes cash flow management and savings. When launching a startup, you never know what can happen and that means that you have to be prepared for the worst possible situation.

In the beginning, it’s generally recommended that you don’t cut off your main source of personal income by quitting your day job to focus your full attention on the startup. While that is preferred and you want to devote as much time as possible to your new venture, you shouldn’t make that move until the business can replace your income.

Furthermore, you need to maintain reserve savings accounts for both yourself and the business in the event of unforeseen emergencies. As we said above, running out of money is the number one cause of failure and the last thing you need is unexpected situations completely draining your operating capital.

Launching a startup can be financially lucrative when done correctly and with the tips above, you can help ensure that you aren’t a statistic for all the wrong reasons. Monitor your cash flow and spending, consider outsourcing and work from home options, and have a “rainy day” fund for any unexpected expenses along the way.